Providing retention incentives is a common and compelling way to entice key employees to stay on board during and after a merger or acquisition. In fact, more than 70% of acquiring companies set aside budgets for retention pools, according to WTW’s 2024 M&A Retention Study. Going forward, however, two important factors could spur even greater use of retention perks:

1. After subdued merger and acquisition (M&A) activity in recent years, observers expect dealmaking to rebound, likely during the remainder of this year and into 2025. If that occurs, it could inspire companies to find creative approaches to retaining key talent affected by these business deals.

2. Recent and future legislation concerning noncompete agreements may make it more difficult for companies to rely on such pacts as M&A binding strategies. While the Federal Trade Commission’s (FTC) attempt to ban these agreements nationwide was struck down by a federal judge in August, many states are pursuing — or in some cases have already instituted — similar bans.

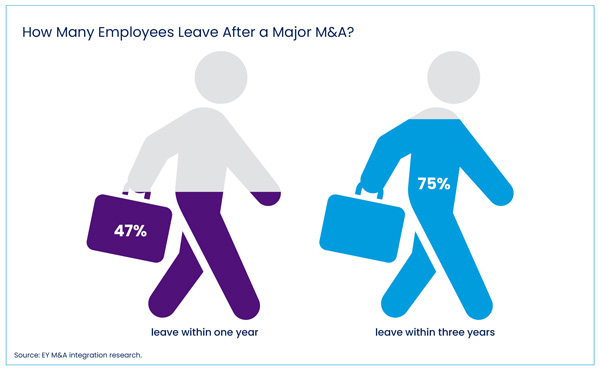

With these factors at play, more employees may be at risk for post-M&A flight — and the number wasn’t small to begin with. Research by EY found that 47% of employees tend to leave their employer within one year of a major M&A transaction and 75% leave within three years. This attrition drain can severely impact productivity and jeopardize deal success.

How can total rewards leaders keep employee churn in check as these potential new developments take hold? Here’s a closer look at expected retention challenges in the M&A environment and the latest guidance on emerging M&A-fueled compensation and benefit strategy shifts.

Corporate M&A deal volume in the U.S. was expected to jump 20% in 2024 and private equity was forecast to rise 16%, according to the EY-Parthenon Deal Barometer, but the rebound has not yet materialized as expected. In fact, a recent M&A outlook update from PwC found that deal volume declined by 25% in the first half of the year versus the same period last year. (Thanks to a few megadeals in the technology and energy sectors, however, deal value was up 5%.)

Elevated interested rates, high valuations and political uncertainty are just some of the factors that have had a chilling effect on M&A activity of late, experts note, and resolution of any of these factors — individually or collectively — could result in a major shift. At the same time, emerging AI technology offers numerous opportunities for investment.

Brian Levy, global deals industry leader and a partner at PwC, believes it’s only a matter of time before the M&A landscape changes. “The lower levels of M&A activity over the past two years have created pent-up demand (and supply), particularly in the private equity (PE) universe,” he wrote in June.

At least one recent report supports that view. A KPMG survey of 200 large corporate and private equity decision-makers revealed optimism about the deal market for the remainder of 2024 and into 2025. Well over half (57%) of respondents expect their next deal will happen this year, while 41% said their next deal will likely happen in 2025. Private equity is particularly bullish about its dealmaking expectations, the survey report found, with 84% saying 2025 will be busier than 2024 and 70% saying 2024 will end up outpacing 2023.

Historically, sale-based noncompete agreements have been used by companies in M&A and PE transactions to keep key employees on board, which is one of the reasons many employers breathed a sigh of relief on Aug. 20 when U.S. District Judge Ada Brown of the Northern District of Texas issued a nationwide injunction on the FTC’s noncompete ban. Though the rule would have carved out an exception for noncompete agreements entered into via a “bona fide” sale of a business, it still had the potential to threaten the use of noncompetes as a M&A tethering tactic. (The FTC defined a bona fide sale as an arm’s-length transaction made between independent parties in which the seller had reasonable chance to negotiate its terms.)

The subject is far from closed, however. The federal government has until Oct. 19, 2024 to appeal the court’s decision. And, even if it doesn’t or the FTC rule never takes effect, restrictions on noncompetes continue to develop at the state level, legal experts note, making it imperative for companies to stay up to date on legislative activity, particularly if they have multistate operations.

Four states — California, Minnesota, North Dakota and Oklahoma — have full bans on noncompete agreements, though the last two carve out exceptions for the dissolution of sale of a business. California’s law is particularly robust, also voiding noncompete agreements entered into in other states. Dozens of other states have partial bans on such agreements based on factors like income level or industry.

Further state action on noncompetes isn’t slowing down, either. Legislatures in Maine, New York and Rhode Island, for example, all passed noncompete bills this year before governors in each state vetoed them, attorneys with Skadden Arps noted, while Washington state recently expanded its rule with some worker-friendly amendments.

“Just as the pandemic forced employers to face the reality of a workforce without offices, unprecedented attention and scrutiny of noncompetes has forced all to consider the possibility of work relationships without restrictive covenants.”

Going forward, law firm Buchanan predicts, state courts and aggressive attorneys general also may challenge overbroad noncompete agreements on a case-by-case basis using states’ antitrust and consumer protection statutes.

If nothing else, attorneys with Jackson Walker wrote, the FTC rule brought a lot of attention to noncompete agreements. “Just as the pandemic forced employers to face the reality of a workforce without offices,” they said, “the rule has forced all to consider the possibility of work relationships without restrictive covenants.”

To comply with noncompete rules and minimize risks of losing key employees, attorneys at Hunton Andrews Kurth recommend that employers take steps now to:

The bottom line is that reliance on employment agreements such as noncompetes, which emphasize the “stick” approach to retaining employees, may shift to retention agreements that instead rely on “carrots” designed to influence the employee’s continued employment through compensation and other enticements.

Bolstering levers such as nonsolicitation, noninterference and nondisclosure provisions still represent options for employers during M&As, noted Josephine Gartrell, J.D., WTW’s senior director, executive compensation and board advisory. But, she acknowledged, balancing financial incentives and engagement efforts with value and competitive protections is essential.

“Shoring up key executives and employees is important to a successful merger or acquisition,” Gartrell said. “To that end, retention agreements play a critical role in keeping talent at target companies both during and after the transaction. The challenge is how to structure retention agreements and determine which executives and employees at the acquired companies should be offered them.”

Companies often conduct criticality analyses in which they group employees into tiers based on how important they are to the success of the organization, she said. Employees in Tier 1, for instance, are considered the most critical to retain. Their value is determined not necessarily by their title, but by the value of their contributions to the organization.

Within these determinations, Gartrell said, there also appears to be some nuanced consideration and increased judgment in play when it comes to tapping retention bonus budgets for payouts. Buyers today are a bit more likely to reserve a portion of the pool (known as dry powder), she notes, in order to discern who among the most critical employees is still a flight risk after the first set of retention awards.

WTW’s 2024 M&A Retention Study charted some important new strategies among the 159 global organizations that responded to the survey.

While time-vested cash bonuses remain the norm, there is an increasing trend toward incorporating performance elements in the calculation, especially for executives and other leaders. Common performance goals include:

Three in 10 organizations offer fixed amounts for M&A retention awards to both senior leadership and salaried employees, according to WTW’s 2024 M&A Retention Study, which gathered data from 159 global organizations.

Within those general practices, however, the actual aggregate and annualized values provided vary substantially depending on company role or job level.

The benchmarks found in WTW’s report?

Most acquiring companies use cash retention bonuses for senior leaders (86%) and other salaried employees (80%), the study notes. Additionally, more than half (56%) use restricted stock or other full-value equity awards for senior leaders, while 40% use these awards for other salaried employees. The retention payment value at the median typically breaks down like this, depending on actual deal value:

More than 1 in 3 companies (35%) award retention agreements or one-time special payments to some of the buyer’s employees, such as those working on the integration of the two companies.

Retention periods typically last between 13 months and 18 months, the report found.

As M&A activity appears poised to ramp up alongside potential new regulatory changes, TR leaders must proactively reevaluate their deal-related retention strategies in terms of carrot versus stick approaches, reassessing what’s likely to be most effective. Balancing financial incentives with strong engagement efforts will be crucial for retaining key personnel throughout the duration of the transactions.

“It’s a new way of looking at things,” Gartrell said, explaining that, along with the financial mechanisms, it’s about customizing and humanizing the transactions as much as possible. Employees need to feel valued, she emphasized — and to see that there are opportunities ahead. That requires communication, especially around why they’re receiving an award.

“If they don’t feel like the outlook for them and their career in whatever transition you’re addressing is positive,” Gartrell said, “then the value sort of becomes inconsequential.”

Workspan freelance writer Lin Grensing-Pophal contributed to this report.

For more information and resources related to this article see the pages below, which offer quick access to all WorldatWork content on these topics: